It is the first Mexican bank with a purely technological base, with a set of hybrid products and services, ideal for managing personal finances in the digital age.

A 100% digital bank is not one that has an application to carry out operations through mobile devices. A true bank of the digital age has, in addition to an efficient platform, products, and services designed for the needs of users of the new normal. Something like the set of benefits that Hey Banco has.

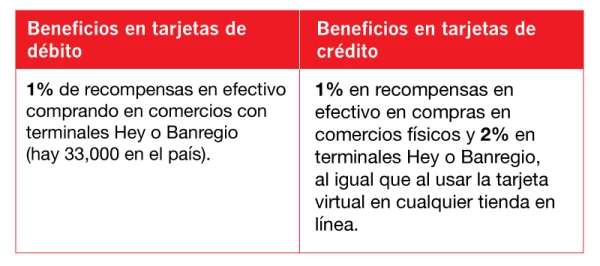

Guaranteed credit cards that do not require prior credit experience, specific cards to make electronic purchases, debit cards to have cash in a network of 12,00 ATMs, rewards programs and the possibility of channeling savings into a global fund are some of the benefits that Hey Banco already offers to its more than 150,000 active clients.

Hey, Banco clients will be able to make deposits in the more than 2,000 BBVA Mexico practices without commissions.

Hey Banco already has more than 12 thousand physical service points nationwide that it offers its users to manage their money through alliances with commercial chains such as 7-Eleven México, affiliated supermarkets of Antad and ATMs available from Banregio, Inbursa, Banbajio and Scotiabank, in order to provide a closer and safer service to all its clients.

“We are building this digital experience in Mexico and we have accelerated growth,” Manuel Rivero Zambrano, CEO of Hey Banco, explained in an interview. “We will become a very relevant bank, being focused on the client to bring the technology of the future.”

Hey Banco benefits

Hey Bank dual card

A 100% digital bankCourtesy Hey Banco

Hey Banco is part of Regional SAB de CV that already has a recognized track record in the banking sector with Banregio. In fact, it was developed in the innovation laboratory of said financial institution, but during the first months of 2020 it operated as an independent business unit due to the growing acceptance of users, mostly made up of professionals and independent workers.

The key to our growth is focused on innovation: our products and services, supported by a robust technological platform, respond to the needs of today’s users

Manuel Rivero Zambrano

Hybrid solutions

Hey Bank has improved its experience in digital banking services. Its app is available on iOS, Android, and AppGallery. Through it, a bank account can be opened in less than five minutes in a totally digital experience.

However, the institution recognizes that although there are transactions that move in the electronic field (and offer all the options) the truth is that there are many operations that are required in the physical world. That is why it has designed a mixed experience: a set of banking services that travel between the electronic environment and the physical space.

For example, if the user requires cash, they can do so, free of charge, at the ATM network that we have already mentioned. You can also go to bank correspondents —7 Eleven, among others— to make payments to credit cards or deposits.

In the same way, you can make interbank transfers and pay or request payments through CoDi, which is activated with QR codes.

Now that if it is about making digital purchases, you have the high-security electronic card to move freely in the world of eCommerce. If you want to pay directly in establishments, you have credit or debit cards, printed on plastic sheets.

As of this May 31, Hey Banco will officially launch rewards for purchases with a debit card; Investment funds; secured credit card; relaunching your traditional credit card; its credit card rewards program, and its 2021 collection cards. Its CEO explained to us the value of these products, which we will review below.

Guaranteed credit card

At Hey Banco you can obtain a credit card even if the applicant does not have a credit history, thanks to its guaranteed option, which is activated as follows: the user deposits from 1,500 pesos as a guarantee, and the bank will issue a card that you will have that amount and up to an additional 20%. If after a semester the client maintains a positive record in handling his card, then the bank evaluates his profile to offer him a Hey Traditional Credit Card.

Neither card handles annuity, both handle very low interest rates and offer reports with suggestions for use for better management.

Cash rewards for your account holders

Within Hey Banco’s innovation discourse is the creation of a benefits system to recognize the good use of the tools it offers to its clients, basically through cash rewards, which becomes an immediate value for users —bye-bye to systems in which you have to accumulate millions of “points” for payments or purchases.

In addition, by opening promotion, it will offer 5% cash rewards on all Credit Card purchases for the next three months.

Your future: grow and export

Saving and investing in Hey Banco is also possible. Its returns are among the most attractive in the market, as it handles a rate of up to 6.5% with investments ranging from 5,000 pesos —in its Inversión Hey product— to participation in a variable income fund that invests in companies in the most developed economies. of the world: Hey Global Fund, which you can enter from with 1,000 pesos.

The bank’s growth has been intense in the last 18 months, as well as its projection for the following years. So the next steps for the institution, in the next five years, according to Manuel Rivero Zambrano, its general director, will be its interconnection with the financial system through APIs that are already well advanced, as well as going beyond borders. Mexican.

(At some point in the next five years) “We will export this digital experience to other countries that use our same protocols. We will share with others this network that we are building ”, concluded Rivero Zambrano.

Hey Bank, is it worth it, or is it a hoax?

Hey bank became a trend for a while in the world of personal finance, but is it really worth it? It was presumed to be the best savings account, so I took on the task of researching it to assess whether it is something worthwhile or not.

To translate video from a foreign language:

Click on the “Settings” icon, select “Subtitles/CC,” and then click “Auto Translate.” A list of languages you can translate into will be displayed. Select “English.”

You’ll see that the subtitles have automatically been translated into English. While everything won’t be translated with 100 percent accuracy, the whole idea is that you can at least get a rough translation so you can easily follow along.

What is Hey Banco?

Before evaluating whether or not Hey Banco is worth it, let’s see what Hey Banco is.

Hey Banco is considered Banregio’s neobank, previously it was known as Sync, today it is called Hey Banco.

If you still don’t know what a neobank is, you can see this: ——

In summary Hey bank is a digital bank that allows you to have a savings account, a debit card and a credit card through an app on your cell phone. So easy, that simple.

Hey Banco is considered a dual card because you have debit and credit in the same place or on the same card, but we’ll talk about this later, I don’t want any confusion.

It has some differentiators such as a guaranteed credit card to create or rebuild your credit history, automatic savings or mobile payment, among others.

Hey bank promised us paradise, he gave it to us for a few months and then he decided to dive into the rocks and he was made shit… ..

What has to be clear is that Hey Banco was for everyone but now it is only for a small group of people and that is what I want to talk about here.

So that you know if it is still a good option or not.

What can you do with your Hey Banco account?

- Open a 100% digital account

- Check the movements from your cell phone

- Make transfers from your cell phone

- Service payments

- Withdraw at ATMs

- Lock and unlock the card

- Set automatic saving

- Invest in 7-day terms

All this from your cell phone and your app

You can also use their website for some things but the app is more convenient.

The Good of Hey Banco

- Ease and speed in opening an account (in 10 minutes you are ready)

- Everything is done from the app. Alloooo

- You can pay with a QR code like any other bank

- You can use your cell phone as if it were a debit card : You can make Spei transfers without problem or use your phone number to receive money instead of using the CLABE

- You can pay credit cards from Banregio or other banks from your cell phone.

- Payments without commissions: Payments to cards, services and Spei transfers have no commissions

- You can set spending limits

- Withdrawal without cards: You can withdraw money at ATMs with your cell phone

- You can use Banregio ATMs without commissions.

- The HeyBanco card allows you to rebuild your credit history.

- There are no account opening or closing costs

- The card is dual (debit and credit at the same time on a single card or account)

- Has the backing of Banregio

- Support and customer service comply

- You can get returns on your savings

- You don’t need average balance

- IPAB protection

- The app is easy to use.

- Protection in the event of death in the amount of $ 25,000 (applies only to active accounts)

The bad thing about Hey Bank

- They charge you between 50 and 70 pesos for Inactivity from the seventh month of inactivity depending on the accounts you use.

- It has a commission for withdrawing at ATMs that are not Banregio or allies (Banregio, Scotiabank, Inbursa and Banbajio).

- The first card is free, from the second, plastic shipments cost 150 pesos

- Cash withdrawal at a foreign ATM 30 pesos

- They have a monthly deposit limit of 3000 Udis (Equivalent to 19,000 pesos) Although this can be unlocked to extend the deposit limit to 10,000 Udis (65,000 pesos approx.)

- The app is not that good yet. It has a lot of usability bugs and still has various issues

- You can’t buy online at all merchants, they have a list of accepted merchants.

- Of the allowed shops in which you can buy online, you can only pay in Dollars

- Branches, if you live in CDMX (there are some ATMs) in Monterrey, quite a few, but outside of there, I only found one in Cancun.

- You cannot buy in dollars, that is, not Amazon US and Paypal (well yes, but with the Paypal rate)

What made it stand out

Hey Banco boasted of being a bank account that did not ask for an average minimum balance, in short they did not ask you to maintain a minimum balance.

Instead they offered that if you voluntarily left a minimum of 3,000 pesos per month, this would generate a yield of 5.5%, if for some reason you did not maintain this balance, nothing happened, they did not charge you commissions and obviously you did not generate returns.

This made Hey Banco acquire users and grow significantly.

Where he watered it

They decided to remove the most important feature, the one I talk about above. Although they still do not ask for minimum balances, your savings no longer generate returns by themselves, now you must invest them for a fixed term of 7 days to be worth it.

Hey Bank is still the best savings account and debit card?

Maybe we can no longer consider it the best but it is still a good opportunity for certain types of people.

Its investment terms are short, its returns are higher than cetes and it continues to evolve so we should still consider it.

Who is the Hey Banco account for?

- For young people looking for their first debit card or savings account who live in Monterrey or have ATMs from banregio, scotiabank and Inbursa present in their life zone.

- For those who have saved more than 10,000 thousand pesos

- People who do not have the habit of saving and need help to do so.

- If you want to rebuild your credit history

Now you know if hey bank is worth it or not. (Depends on your profile)

How safe is Hey Bank?

It is just as safe as any other large bank such as Banregio, BBVA, Santander, etc.

Hey Banco has IPAB Protection and is supervised by Condusef . In other words, they are supervised by the government and guarantee the safety of your money for up to 400,000 Udis.

Any problem you have you can approach the Condusef for help.

If we talk about security, hey bank is worth it and there is no need to worry.

Source: milenio.com, expansion.mx, finanzasm.com, heybanco.com

{kind=link}